Cocoa & Chocolate Market Synopsis

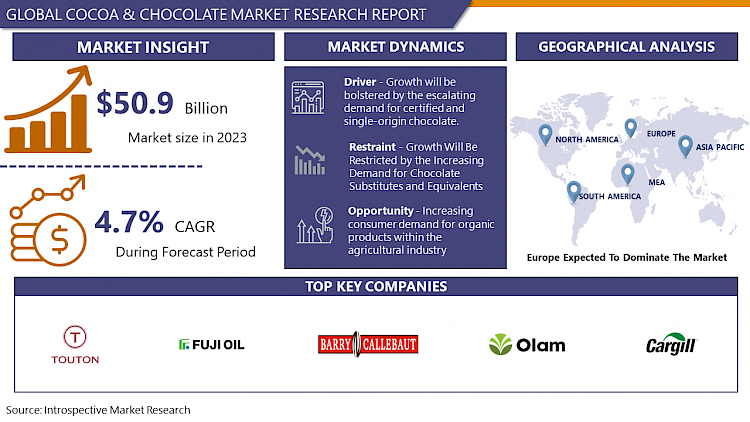

The Cocoa & Chocolate Market Size Was Valued at USD 50.9 Billion in 2023, and is Projected to Reach USD 77.0 Billion by 2032, Growing at a CAGR of 4.7% From 2024-2032.

Cocoa is chocolate in its purest form. Chocolate is produced using the same manufacturing process as cocoa, which involves the transformation of cocoa pods. Cocoa butter is not, nevertheless, extracted from chocolate. The silkiness and opulence of chocolate are attributed to cocoa butter.

After the cocoa butter has been extracted, a portion of the roasted bean fragments is ground into cocoa powder. The majority of cocoa-based product manufacturing processes utilize cocoa powder, including the production of beverages, confection fillings, ice creams, and more. Customers can generally obtain cocoa powder from retail establishments. The solid form of chocolate is produced through the combination of cocoa butter, cocoa fluid, and sugar. Chocolate's darkness is determined by the amount of cocoa liquor incorporated into the final product. The large caloric, fat, and sugar content of chocolate is attributable to cocoa butter. There are numerous varieties of chocolate, such as unsweetened, semisweet, sweet, dark, milk, white, and compound. There are numerous varieties of chocolate, such as bars, tiny beads, liquid, and powder. The expansion of the cocoa and chocolate industry is being propelled by heightened holiday sales, expanded utilization of chocolate as a functional food, and increased implementation of dark and ruby chocolate. The rising popularity of chocolate as a holiday gift has contributed to an increase in chocolate demand. In contemporary society, chocolate celebrations are favored as presents due to their extensive selection of flavors and price points.

- Cocoa is a substance produced from cocoa tree kernels. Cocoa, which originated in Asia and Oceania, has since spread to nearly every tropical region, including West and Central Africa and Africa. A variety of products are manufactured from cocoa seeds, including cocoa liquor, cocoa butter, and cocoa flour.

- The market is experiencing consistent expansion as a result of the worldwide chocolate confectionery industry's robust growth trajectory. The origin proportion of worldwide grindings has increased substantially, resulting in a surge in the consumption of cocoa-based ingredients worldwide.

- Additionally, new product developments in various sectors of the culinary industry contribute to the expansion of the cocoa and chocolate market. The flavor of chocolate has continued to be the most introduced in the beverage, confectionary, and confectionery industries. Additionally, it continues to be a prevalent ingredient in the confectionery and beverage industries. It is anticipated that this industry trend will propel market expansion for the foreseeable future.

Cocoa & Chocolate Market Trend Analysis

Increased demand for chocolate confections will propel market expansion.

- The worldwide market for cocoa and chocolate is predominantly driven by the rising demand for chocolate confectionery. In recent years, emerging economies have witnessed an increase in the demand for chocolate confectioneries, which can be attributed to increasing consumer spending on indulgent confectionery products, particularly chocolate confectioneries. It is anticipated that the increasing desire for molded and countline chocolates in developed economies will have a positive impact on the chocolate confectionery industry.

- The development of this industry is anticipated to be facilitated by the addition of new chocolate varieties to the portfolios of key manufacturers, including dark chocolate and ruby chocolate. Additionally, the increasing practice of bestowing chocolates as gifts during the holiday season is anticipated to significantly contribute to the chocolate confectionery market's expansion over the forecast period.

Supportive Demand for Specialty Chocolate Products to Encourage Progress and Innovation

- In recent years, there has been a noticeable surge in the desire for a premium or specialty chocolates, particularly in developed nations such as the United States, France, Belgium, and Germany. It is anticipated that there will be a progressive increase in the forthcoming years. A chief motivator is the growing inclination of consumers to ascertain the provenance of every ingredient utilized in chocolate products. It can be caused by a variety of factors, including vegan preferences and lactose intolerance of specific components. Additionally, products crafted from organic cocoa seeds are in high demand. These elements are anticipated to promote the expansion of specialty chocolates.

- The growing preference for organic and clean-label products as a means to promote holistic health and well-being has resulted in an elevated need for dark and sugar-free chocolates. In the coming years, the growing consciousness surrounding labor welfare is anticipated to contribute to the continued surge in demand for fair-traded cocoa.

Cocoa & Chocolate Market Segment Analysis:

Cocoa & Chocolate Market Segmented based on type, product, nature, applications, and distribution channels.

By product, the traditional segment is expected to dominate the market during the forecast period

- The market is anticipated to be dominated by the traditional segment throughout the forecast period. White chocolate, milk chocolate, and dark chocolate are included. The increased accessibility, popularity, and market penetration of cocoa in comparison to carob, the raw material utilized in artificial chocolate, account for this phenomenon. Given its early entry into the market, milk chocolate is the prevailing variety among the diverse range of traditional chocolates.

- The CAGR for artificial chocolate is anticipated to be the highest during the forecast period. The exponential expansion can be ascribed to the absence of caffeine in carob candies, which renders them appropriate for individuals who are sensitive to caffeine. Furthermore, carob contains nearly three times as much calcium as cocoa. This contributes to its widespread appeal, especially among women and individuals suffering from calcium deficiencies.

By application, the Food and beverages segment held the largest share in 2023

- The demand for cocoa and chocolate is anticipated to increase in tandem with rising consumer health consciousness and rising consumption of confectionary items such as chocolate-infused cookies, doughnuts, cupcakes, rolls, sweet rolls, cakes, pies, and coffee cakes.

- Increasing demand within the beverage industry is also anticipated to contribute to the expansion of the market. The demand is predominantly determined by consumer preference in beverage selection, which is significantly impacted by the flavor profile of the beverage. Diverse product offerings, including chocolate syrups and chocolate-infused alcoholic beverages, are expanding the market's selection of cocoa-based beverages, thereby contributing to the segment's expansion. This, in conjunction with increasing the cocoa content to decrease the sugar content of a beverage, enables previously untapped consumer segments to prefer chocolate beverages to those sweetened artificially.

Cocoa & Chocolate Market Regional Insights:

Europe is Expected to Dominate the Market Over the Forecast period

- The European market is the greatest producer of chocolate on a global scale and one of the largest importers of cocoa. Increasing consumer preference for chocolates over other delicacies for celebrations and health-conscious consumption, as well as a rising consumer trend toward niche chocolates such as the bean-to-bar concept of chocolates from a singular origin, are driving market expansion. This, coupled with the availability of a wide variety of cocoa yields in Europe, has encouraged chocolate manufacturers to enter the premium chocolate sector and develop specialized products.

- It is expected that Europe will experience a rise in the demand for cocoa and chocolate due to the existence of established market participants. Additionally, Europe is a significant cacao producer. This is anticipated to stimulate the expansion of the regional market.

- The market is anticipated to be dominated by North America throughout the forecast period. The increasing demand for chocolate in North America is concurrently propelling the expansion of cocoa in the area, given that cocoa serves as the primary basic material in the chocolate manufacturing process. Furthermore, the escalating consumer demand for chocolate generates a corresponding need for cocoa butter, which imparts the chocolate with its delectable texture.

Active Key Players in the Cocoa & Chocolate Market

- Barry Callebaut, AG (Switzerland)

- Cargill, Inc. (U.S.)

- Olam International (Singapore)

- Fuji Oil Company Ltd. (Japan)

- ECOM Agroindustrial Corporation Ltd. (Switzerland)

- Cocoa Processing Co. Ltd. (Ghana)

- Touton S.A. (France)

- Niche Cocoa Industry Ltd. (Ghana)

- BD Associates Ghana Ltd. (Ghana)

- PLOT Enterprise Ghana Limited (Ghana), and Other Key Players

Key Industry Developments in the Cocoa & Chocolate Market:

- Barry Callebaut declared the enlargement of its Campbellfield, Melbourne, Australia facility in March 2022. Producing safe, high-quality goods, the new factory broadens the organization's presence in the Asia-Pacific region. The facility is capable of catering to the entire food industry in Australia, including both local and international food manufacturers, artisanal chocolate consumers, and professionals.

|

Global Cocoa & Chocolate Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 50.9 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.7 % |

Market Size in 2032: |

USD 77.0 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Product |

|

||

|

By Nature |

|

||

|

By Application |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

- INTRODUCTION

- RESEARCH OBJECTIVES

- RESEARCH METHODOLOGY

- RESEARCH PROCESS

- SCOPE AND COVERAGE

- Market Definition

- Key Questions Answered

- MARKET SEGMENTATION

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GROWTH OPPORTUNITIES BY SEGMENT

- MARKET LANDSCAPE

- PORTER’S FIVE FORCES ANALYSIS

- Bargaining Power Of Supplier

- Threat Of New Entrants

- Threat Of Substitutes

- Competitive Rivalry

- Bargaining Power Among Buyers

- INDUSTRY VALUE CHAIN ANALYSIS

- MARKET DYNAMICS

- Drivers

- Restraints

- Opportunities

- Challenges

- MARKET TREND ANALYSIS

- REGULATORY LANDSCAPE

- PESTLE ANALYSIS

- PRICE TREND ANALYSIS

- PATENT ANALYSIS

- TECHNOLOGY EVALUATION

- MARKET IMPACT OF THE RUSSIA-UKRAINE WAR

- Geopolitical Market Disruptions

- Supply Chain Disruptions

- Instability in Emerging Markets

- ECOSYSTEM

- PORTER’S FIVE FORCES ANALYSIS

- COCOA & CHOCOLATE MARKET BY TYPE (2017-2032)

- COCOA & CHOCOLATE MARKET SNAPSHOT AND GROWTH ENGINE

- MARKET OVERVIEW

- COCOA BUTTER

- Introduction And Market Overview

- Historic And Forecasted Market Size in Value (2017 – 2032F)

- Historic And Forecasted Market Size in Volume (2017 – 2032F)

- Key Market Trends, Growth Factors And Opportunities

- Geographic Segmentation Analysis

- COCOA POWDER

- COCOA LIQUOR

- COCOA & CHOCOLATE MARKET BY PRODUCT (2017-2032)

- COCOA & CHOCOLATE MARKET SNAPSHOT AND GROWTH ENGINE

- MARKET OVERVIEW

- TRADITIONAL

- Introduction And Market Overview

- Historic And Forecasted Market Size in Value (2017 – 2032F)

- Historic And Forecasted Market Size in Volume (2017 – 2032F)

- Key Market Trends, Growth Factors And Opportunities

- Geographic Segmentation Analysis

- ARTIFICIAL

- COCOA & CHOCOLATE MARKET BY NATURE (2017-2032)

- COCOA & CHOCOLATE MARKET SNAPSHOT AND GROWTH ENGINE

- MARKET OVERVIEW

- ORGANIC

- Introduction And Market Overview

- Historic And Forecasted Market Size in Value (2017 – 2032F)

- Historic And Forecasted Market Size in Volume (2017 – 2032F)

- Key Market Trends, Growth Factors And Opportunities

- Geographic Segmentation Analysis

- CONVENTIONAL

- COCOA & CHOCOLATE MARKET BY APPLICATION (2017-2032)

- COCOA & CHOCOLATE MARKET SNAPSHOT AND GROWTH ENGINE

- MARKET OVERVIEW

- CONFECTIONERY

- Introduction And Market Overview

- Historic And Forecasted Market Size in Value (2017 – 2032F)

- Historic And Forecasted Market Size in Volume (2017 – 2032F)

- Key Market Trends, Growth Factors And Opportunities

- Geographic Segmentation Analysis

- FOOD AND BEVERAGES

- BAKERY

- PHARMA

- ANIMAL FEED

- OTHERS

- COCOA & CHOCOLATE MARKET BY DISTRIBUTION CHANNEL (2017-2032)

- COCOA & CHOCOLATE MARKET SNAPSHOT AND GROWTH ENGINE

- MARKET OVERVIEW

- SUPERMARKET & HYPERMARKETS

- Introduction And Market Overview

- Historic And Forecasted Market Size in Value (2017 – 2032F)

- Historic And Forecasted Market Size in Volume (2017 – 2032F)

- Key Market Trends, Growth Factors And Opportunities

- Geographic Segmentation Analysis

- CONVENIENCE STORES

- ONLINE

- COMPANY PROFILES AND COMPETITIVE ANALYSIS

- COMPETITIVE LANDSCAPE

- Competitive Positioning

- Cocoa & Chocolate Market Share By Manufacturer (2023)

- Industry BCG Matrix

- Heat Map Analysis

- Mergers & Acquisitions

- BARRY CALLEBAUT, AG (SWITZERLAND)

- Company Overview

- Key Executives

- Company Snapshot

- Role of the Company in the Market

- Sustainability and Social Responsibility

- Operating Business Segments

- Product Portfolio

- Business Performance (Production Volume, Sales Volume, Sales Margin, Production Capacity, Capacity Utilization Rate)

- Key Strategic Moves And Recent Developments

- SWOT Analysis

- CARGILL, INC. (U.S.)

- OLAM INTERNATIONAL (SINGAPORE)

- FUJI OIL COMPANY LTD. (JAPAN)

- ECOM AGROINDUSTRIAL CORPORATION LTD. (SWITZERLAND)

- COCOA PROCESSING CO. LTD. (GHANA)

- TOUTON S.A. (FRANCE)

- NICHE COCOA INDUSTRY LTD. (GHANA)

- BD ASSOCIATES GHANA LTD. (GHANA)

- PLOT ENTERPRISE GHANA LIMITED (GHANA)

- COMPETITIVE LANDSCAPE

- GLOBAL COCOA & CHOCOLATE MARKET BY REGION

- OVERVIEW

- NORTH AMERICA

- Key Market Trends, Growth Factors And Opportunities

- Key Manufacturers

- Historic And Forecasted Market Size By Type

- Historic And Forecasted Market Size By Product

- Historic And Forecasted Market Size By Nature

- Historic And Forecasted Market Size By Application

- Historic And Forecasted Market Size By Distribution Channel

- Historic And Forecasted Market Size By Country

- USA

- Canada

- Mexico

- EASTERN EUROPE

- Key Market Trends, Growth Factors And Opportunities

- Key Manufacturers

- Historic And Forecasted Market Size By Segments

- Historic And Forecasted Market Size By Country

- Russia

- Bulgaria

- The Czech Republic

- Hungary

- Poland

- Romania

- Rest Of Eastern Europe

- WESTERN EUROPE

- Key Market Trends, Growth Factors And Opportunities

- Key Manufacturers

- Historic And Forecasted Market Size By Segments

- Historic And Forecasted Market Size By Country

- Germany

- United Kingdom

- France

- The Netherlands

- Italy

- Spain

- Rest Of Western Europe

- ASIA PACIFIC

- Key Market Trends, Growth Factors And Opportunities

- Key Manufacturers

- Historic And Forecasted Market Size By Segments

- Historic And Forecasted Market Size By Country

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Vietnam

- The Philippines

- Australia

- New-Zealand

- Rest Of APAC

- MIDDLE EAST & AFRICA

- Key Market Trends, Growth Factors And Opportunities

- Key Manufacturers

- Historic And Forecasted Market Size By Segments

- Historic And Forecasted Market Size By Country

- Turkey

- Bahrain

- Kuwait

- Saudi Arabia

- Qatar

- UAE

- Israel

- South Africa

- SOUTH AMERICA

- Key Market Trends, Growth Factors And Opportunities

- Key Manufacturers

- Historic And Forecasted Market Size By Segments

- Historic And Forecasted Market Size By Country

- Brazil

- Argentina

- Rest of South America

- INVESTMENT ANALYSIS

- ANALYST VIEWPOINT AND CONCLUSION

- Recommendations and Concluding Analysis

- Potential Market Strategies

|

Global Cocoa & Chocolate Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 50.9 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.7 % |

Market Size in 2032: |

USD 77.0 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Product |

|

||

|

By Nature |

|

||

|

By Application |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

LIST OF TABLES

TABLE 001. EXECUTIVE SUMMARY

TABLE 002. COCOA & CHOCOLATE MARKET BARGAINING POWER OF SUPPLIERS

TABLE 003. COCOA & CHOCOLATE MARKET BARGAINING POWER OF CUSTOMERS

TABLE 004. COCOA & CHOCOLATE MARKET COMPETITIVE RIVALRY

TABLE 005. COCOA & CHOCOLATE MARKET THREAT OF NEW ENTRANTS

TABLE 006. COCOA & CHOCOLATE MARKET THREAT OF SUBSTITUTES

TABLE 007. COCOA & CHOCOLATE MARKET BY TYPE

TABLE 008. COCOA {COCOA POWDER MARKET OVERVIEW (2016-2028)

TABLE 009. COCOA BUTTER MARKET OVERVIEW (2016-2028)

TABLE 010. COCOA LIQUOR MARKET OVERVIEW (2016-2028)

TABLE 011. OTHERS} MARKET OVERVIEW (2016-2028)

TABLE 012. CHOCOLATE {DARK MARKET OVERVIEW (2016-2028)

TABLE 013. WHITE MARKET OVERVIEW (2016-2028)

TABLE 014. MILK MARKET OVERVIEW (2016-2028)

TABLE 015. FILLED} MARKET OVERVIEW (2016-2028)

TABLE 016. COCOA & CHOCOLATE MARKET BY APPLICATION

TABLE 017. FOOD & BEVERAGES MARKET OVERVIEW (2016-2028)

TABLE 018. COSMETICS MARKET OVERVIEW (2016-2028)

TABLE 019. PHARMACEUTICALS MARKET OVERVIEW (2016-2028)

TABLE 020. OTHERS MARKET OVERVIEW (2016-2028)

TABLE 021. NORTH AMERICA COCOA & CHOCOLATE MARKET, BY TYPE (2016-2028)

TABLE 022. NORTH AMERICA COCOA & CHOCOLATE MARKET, BY APPLICATION (2016-2028)

TABLE 023. N COCOA & CHOCOLATE MARKET, BY COUNTRY (2016-2028)

TABLE 024. EUROPE COCOA & CHOCOLATE MARKET, BY TYPE (2016-2028)

TABLE 025. EUROPE COCOA & CHOCOLATE MARKET, BY APPLICATION (2016-2028)

TABLE 026. COCOA & CHOCOLATE MARKET, BY COUNTRY (2016-2028)

TABLE 027. ASIA PACIFIC COCOA & CHOCOLATE MARKET, BY TYPE (2016-2028)

TABLE 028. ASIA PACIFIC COCOA & CHOCOLATE MARKET, BY APPLICATION (2016-2028)

TABLE 029. COCOA & CHOCOLATE MARKET, BY COUNTRY (2016-2028)

TABLE 030. MIDDLE EAST & AFRICA COCOA & CHOCOLATE MARKET, BY TYPE (2016-2028)

TABLE 031. MIDDLE EAST & AFRICA COCOA & CHOCOLATE MARKET, BY APPLICATION (2016-2028)

TABLE 032. COCOA & CHOCOLATE MARKET, BY COUNTRY (2016-2028)

TABLE 033. SOUTH AMERICA COCOA & CHOCOLATE MARKET, BY TYPE (2016-2028)

TABLE 034. SOUTH AMERICA COCOA & CHOCOLATE MARKET, BY APPLICATION (2016-2028)

TABLE 035. COCOA & CHOCOLATE MARKET, BY COUNTRY (2016-2028)

TABLE 036. ADM: SNAPSHOT

TABLE 037. ADM: BUSINESS PERFORMANCE

TABLE 038. ADM: PRODUCT PORTFOLIO

TABLE 039. ADM: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 039. CARGILL: SNAPSHOT

TABLE 040. CARGILL: BUSINESS PERFORMANCE

TABLE 041. CARGILL: PRODUCT PORTFOLIO

TABLE 042. CARGILL: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 042. BARRY CALLEBAUT: SNAPSHOT

TABLE 043. BARRY CALLEBAUT: BUSINESS PERFORMANCE

TABLE 044. BARRY CALLEBAUT: PRODUCT PORTFOLIO

TABLE 045. BARRY CALLEBAUT: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 045. PLOT GHANA: SNAPSHOT

TABLE 046. PLOT GHANA: BUSINESS PERFORMANCE

TABLE 047. PLOT GHANA: PRODUCT PORTFOLIO

TABLE 048. PLOT GHANA: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 048. DUTCH COCOA: SNAPSHOT

TABLE 049. DUTCH COCOA: BUSINESS PERFORMANCE

TABLE 050. DUTCH COCOA: PRODUCT PORTFOLIO

TABLE 051. DUTCH COCOA: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 051. COCOA PROCESSING COMPANY LIMITED: SNAPSHOT

TABLE 052. COCOA PROCESSING COMPANY LIMITED: BUSINESS PERFORMANCE

TABLE 053. COCOA PROCESSING COMPANY LIMITED: PRODUCT PORTFOLIO

TABLE 054. COCOA PROCESSING COMPANY LIMITED: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 054. INDCRESA: SNAPSHOT

TABLE 055. INDCRESA: BUSINESS PERFORMANCE

TABLE 056. INDCRESA: PRODUCT PORTFOLIO

TABLE 057. INDCRESA: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 057. BLOMMER: SNAPSHOT

TABLE 058. BLOMMER: BUSINESS PERFORMANCE

TABLE 059. BLOMMER: PRODUCT PORTFOLIO

TABLE 060. BLOMMER: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 060. JB FOODS LIMITED: SNAPSHOT

TABLE 061. JB FOODS LIMITED: BUSINESS PERFORMANCE

TABLE 062. JB FOODS LIMITED: PRODUCT PORTFOLIO

TABLE 063. JB FOODS LIMITED: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 063. BUNGE: SNAPSHOT

TABLE 064. BUNGE: BUSINESS PERFORMANCE

TABLE 065. BUNGE: PRODUCT PORTFOLIO

TABLE 066. BUNGE: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 066. UNITED COCOA PROCESSOR INC: SNAPSHOT

TABLE 067. UNITED COCOA PROCESSOR INC: BUSINESS PERFORMANCE

TABLE 068. UNITED COCOA PROCESSOR INC: PRODUCT PORTFOLIO

TABLE 069. UNITED COCOA PROCESSOR INC: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 069. CEMOI: SNAPSHOT

TABLE 070. CEMOI: BUSINESS PERFORMANCE

TABLE 071. CEMOI: PRODUCT PORTFOLIO

TABLE 072. CEMOI: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 072. EUROMAR COMMODITIES GMBH: SNAPSHOT

TABLE 073. EUROMAR COMMODITIES GMBH: BUSINESS PERFORMANCE

TABLE 074. EUROMAR COMMODITIES GMBH: PRODUCT PORTFOLIO

TABLE 075. EUROMAR COMMODITIES GMBH: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 075. NESTLE: SNAPSHOT

TABLE 076. NESTLE: BUSINESS PERFORMANCE

TABLE 077. NESTLE: PRODUCT PORTFOLIO

TABLE 078. NESTLE: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 078. OLAM: SNAPSHOT

TABLE 079. OLAM: BUSINESS PERFORMANCE

TABLE 080. OLAM: PRODUCT PORTFOLIO

TABLE 081. OLAM: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 081. DANDELION CHOCOLATE: SNAPSHOT

TABLE 082. DANDELION CHOCOLATE: BUSINESS PERFORMANCE

TABLE 083. DANDELION CHOCOLATE: PRODUCT PORTFOLIO

TABLE 084. DANDELION CHOCOLATE: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 084. FUJI OIL: SNAPSHOT

TABLE 085. FUJI OIL: BUSINESS PERFORMANCE

TABLE 086. FUJI OIL: PRODUCT PORTFOLIO

TABLE 087. FUJI OIL: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 087. GUITTARD CHOCOLATE: SNAPSHOT

TABLE 088. GUITTARD CHOCOLATE: BUSINESS PERFORMANCE

TABLE 089. GUITTARD CHOCOLATE: PRODUCT PORTFOLIO

TABLE 090. GUITTARD CHOCOLATE: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 090. MONDELEZ: SNAPSHOT

TABLE 091. MONDELEZ: BUSINESS PERFORMANCE

TABLE 092. MONDELEZ: PRODUCT PORTFOLIO

TABLE 093. MONDELEZ: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 093. PURATOS: SNAPSHOT

TABLE 094. PURATOS: BUSINESS PERFORMANCE

TABLE 095. PURATOS: PRODUCT PORTFOLIO

TABLE 096. PURATOS: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 096. IRCA: SNAPSHOT

TABLE 097. IRCA: BUSINESS PERFORMANCE

TABLE 098. IRCA: PRODUCT PORTFOLIO

TABLE 099. IRCA: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 099. WUXI HUADONG: SNAPSHOT

TABLE 100. WUXI HUADONG: BUSINESS PERFORMANCE

TABLE 101. WUXI HUADONG: PRODUCT PORTFOLIO

TABLE 102. WUXI HUADONG: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 102. SHANGHAI GOLDEN MONGKEY: SNAPSHOT

TABLE 103. SHANGHAI GOLDEN MONGKEY: BUSINESS PERFORMANCE

TABLE 104. SHANGHAI GOLDEN MONGKEY: PRODUCT PORTFOLIO

TABLE 105. SHANGHAI GOLDEN MONGKEY: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 105. CHANGZHOU XIANGER: SNAPSHOT

TABLE 106. CHANGZHOU XIANGER: BUSINESS PERFORMANCE

TABLE 107. CHANGZHOU XIANGER: PRODUCT PORTFOLIO

TABLE 108. CHANGZHOU XIANGER: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 108. QINGDAO JIANA: SNAPSHOT

TABLE 109. QINGDAO JIANA: BUSINESS PERFORMANCE

TABLE 110. QINGDAO JIANA: PRODUCT PORTFOLIO

TABLE 111. QINGDAO JIANA: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 111. SHANGHAI NAJIA: SNAPSHOT

TABLE 112. SHANGHAI NAJIA: BUSINESS PERFORMANCE

TABLE 113. SHANGHAI NAJIA: PRODUCT PORTFOLIO

TABLE 114. SHANGHAI NAJIA: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 114. SHAOXING QILI XINGGUANG: SNAPSHOT

TABLE 115. SHAOXING QILI XINGGUANG: BUSINESS PERFORMANCE

TABLE 116. SHAOXING QILI XINGGUANG: PRODUCT PORTFOLIO

TABLE 117. SHAOXING QILI XINGGUANG: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 117. JIANGSU LINZHI SHANGYANG: SNAPSHOT

TABLE 118. JIANGSU LINZHI SHANGYANG: BUSINESS PERFORMANCE

TABLE 119. JIANGSU LINZHI SHANGYANG: PRODUCT PORTFOLIO

TABLE 120. JIANGSU LINZHI SHANGYANG: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 120. OTHER MAJOR PLAYERS: SNAPSHOT

TABLE 121. OTHER MAJOR PLAYERS: BUSINESS PERFORMANCE

TABLE 122. OTHER MAJOR PLAYERS: PRODUCT PORTFOLIO

TABLE 123. OTHER MAJOR PLAYERS: KEY STRATEGIC MOVES AND DEVELOPMENTS

LIST OF FIGURES

FIGURE 001. YEARS CONSIDERED FOR ANALYSIS

FIGURE 002. SCOPE OF THE STUDY

FIGURE 003. COCOA & CHOCOLATE MARKET OVERVIEW BY REGIONS

FIGURE 004. PORTER'S FIVE FORCES ANALYSIS

FIGURE 005. BARGAINING POWER OF SUPPLIERS

FIGURE 006. COMPETITIVE RIVALRYFIGURE 007. THREAT OF NEW ENTRANTS

FIGURE 008. THREAT OF SUBSTITUTES

FIGURE 009. VALUE CHAIN ANALYSIS

FIGURE 010. PESTLE ANALYSIS

FIGURE 011. COCOA & CHOCOLATE MARKET OVERVIEW BY TYPE

FIGURE 012. COCOA {COCOA POWDER MARKET OVERVIEW (2016-2028)

FIGURE 013. COCOA BUTTER MARKET OVERVIEW (2016-2028)

FIGURE 014. COCOA LIQUOR MARKET OVERVIEW (2016-2028)

FIGURE 015. OTHERS} MARKET OVERVIEW (2016-2028)

FIGURE 016. CHOCOLATE {DARK MARKET OVERVIEW (2016-2028)

FIGURE 017. WHITE MARKET OVERVIEW (2016-2028)

FIGURE 018. MILK MARKET OVERVIEW (2016-2028)

FIGURE 019. FILLED} MARKET OVERVIEW (2016-2028)

FIGURE 020. COCOA & CHOCOLATE MARKET OVERVIEW BY APPLICATION

FIGURE 021. FOOD & BEVERAGES MARKET OVERVIEW (2016-2028)

FIGURE 022. COSMETICS MARKET OVERVIEW (2016-2028)

FIGURE 023. PHARMACEUTICALS MARKET OVERVIEW (2016-2028)

FIGURE 024. OTHERS MARKET OVERVIEW (2016-2028)

FIGURE 025. NORTH AMERICA COCOA & CHOCOLATE MARKET OVERVIEW BY COUNTRY (2016-2028)

FIGURE 026. EUROPE COCOA & CHOCOLATE MARKET OVERVIEW BY COUNTRY (2016-2028)

FIGURE 027. ASIA PACIFIC COCOA & CHOCOLATE MARKET OVERVIEW BY COUNTRY (2016-2028)

FIGURE 028. MIDDLE EAST & AFRICA COCOA & CHOCOLATE MARKET OVERVIEW BY COUNTRY (2016-2028)

FIGURE 029. SOUTH AMERICA COCOA & CHOCOLATE MARKET OVERVIEW BY COUNTRY (2016-2028)

Frequently Asked Questions :

The forecast period in the Cocoa & Chocolate Market research report is 2024-2032.

Barry Callebaut, AG (Switzerland) Cargill, Inc. (U.S.) Olam International (Singapore) Fuji Oil Company Ltd. (Japan) ECOM Agroindustrial Corporation Ltd. (Switzerland) Cocoa Processing Co. Ltd. (Ghana) Touton S.A. (France) Niche Cocoa Industry Ltd. (Ghana) BD Associates Ghana Ltd. (Ghana) PLOT Enterprise Ghana Limited (Ghana), and Other Major Players.

The Cocoa & Chocolate Market is segmented into type, product, nature, applications, distribution channels, and region. By type, the market is categorized into Cocoa Butter, Cocoa Powder, and Cocoa Liquor. By product, the market is categorized into Traditional and Artificial. By nature, the market is categorized into Organic and Conventional. By applications, the market is categorized into Confectionery, Food and beverages, Bakery, Pharma, Animal Feed, and Others. By distribution channels, the market is categorized into Supermarket & Hypermarkets, Convenience Stores, and Online. By region, it is analyzed across North America (U.S.; Canada; Mexico), Europe (Germany; U.K.; France; Italy; Russia; Spain, etc.), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

Cocoa is a pure and unaltered variety of chocolate. Chocolate, which is produced from cocoa seeds, undergoes the same manufacturing process as cocoa. Nevertheless, cocoa butter remains in chocolate. Cocoa butter enhances the velvety and opulent texture of chocolate.

The Cocoa & Chocolate Market Size Was Valued at USD 50.9 Billion in 2023, and is Projected to Reach USD 77.0 Billion by 2032, Growing at a CAGR of 4.7% From 2024-2032.