Hereditary Orotic Aciduria Market Synopsis:

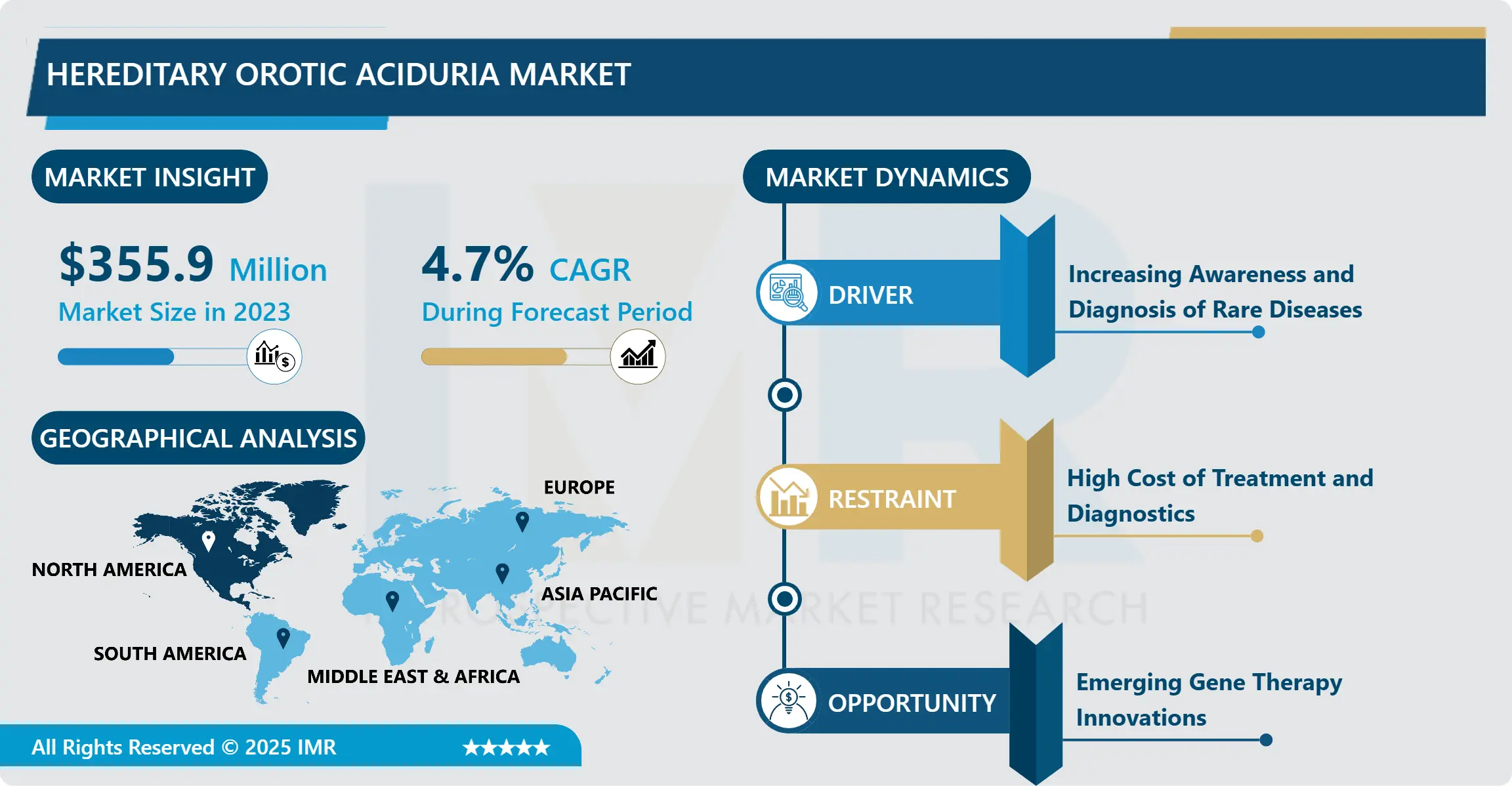

Hereditary Orotic Aciduria Market Size Was Valued at USD 355.9 Million in 2023 and is Projected to Reach USD 538.08 Million by 2032, Growing at a CAGR of 4.7% From 2024-2032.

Hereditary Orotic Aciduria is a rare metabolic disease caused by the OMIM database the UMPS gene inheritance of recessive nature of the pyrimidine biosynthesis de novo pathway, the enzyme deficiency. This enzyme catalyzes the conversion of orotic acid to uridine monophosphate (UMP), which is needed in pyrimidine synthesis; pyrimidines are parts of both DNA and RNA. In patients with hereditary orotic aciduria, this causing an enzymatic block leads to the deposition of orotic acid in the body fluids and typical clinical symptoms such as megaloblastic anemia, impaired growth, developmental delays, and crystalluria of orotic acid in the urine. The market for hereditary orotic aciduria is valued as there is a rising understanding of rare genetic diseases, enhanced genetic analysis possibilities, and the introduction of unique treatments for hereditary orotic aciduria, such as uridine which is an alternative pathway to overcome the metabolic block.

Based on the hereditary form, the orotic aciduria market forms a small portion of the rare genetic disorders market, but has a good potential for growth due to perspicuous awareness, strict genetic screening, and growth in therapeutic products.. HI, hereditary orotic aciduria is an uncommon autosomal logger juvenile disease anger Relations with an enzymatic insufficiency that impairs the pyrimidine biosynthesis process causing an increased concentration of orotic acid. This condition is characterized by Megaloblastic anaemias, developmental disorders, growth impairment, and abnormalities in the urinary systems, and therefore needs the services of a pediatrician and other professional medical officers. With increasing concern in metabolic disorders, the need to diagnose, as well as to treat, hereditary orotic aciduria has heightened in areas with developed networks such as North America, Europe, and Asia-Pacific.

The growth of hereditary orotic aciduria has a strong backing from accessibility to treatments such as supplements of uridine which provides a workaround effect to the blocks created by the missing enzyme. This market is also supported by consistencies of orphan drug regulations and policies, which offer bureaucratic and fiscal encouragement to pharmaceutical firms for exclusive medical product development for rare diseases. Leading stakeholders are making efforts to grow patient registries, clinical trials and partnerships with government and nongovernment organizations to develop therapeutic interventions.

Hereditary Orotic Aciduria Market Trend Analysis:

Increasing Emphasis on Genetic and Newborn Screening Programs

-

Another conspicuous tendency in the hereditary orotic aciduria market is the increasing attention being paid to the genetic and newborn screening services that would help identify and provide early treatment of the cases of RMDS. Due to changes in genetic technologies and sequencing, healthcare providers as well as researchers have come up with high to diagnose genetic conditions at the beginning of birth hence providing better chances for disease control. Newborn screening has become popular in developed countries because such governments and health systems promote comprehensive screening practices. Furthermore, with the existing population of families at risk of having children with hereditary diseases, there are specially organized genetic counselling services aimed at helping the client clarify the genetic risks and potential consequences of the further transmission of a particular gene.

Growing Demand for Orphan Drugs and Regulatory Support

-

The hereditary orotic aciduria market is considered as a niche market because it deals with the orphan drugs and now it has an immense prospect owing to the regulations falling in place for the development and provision of the Rare Diseases. International governments and other regulatory agencies such as North American and European counterparts offer grants and tax-cutting policies to spur investment in orphan drugs for diseases rarely affecting the populace, but necessitating unique treatments like hereditary orotic aciduria. For example, the U.S. FDA and European Medicines Agency (EMA) offer programs including market exclusivity for certain drugs, fast-track approval, and reduced fees that significantly decreases financial and regulatory costs to organizations developing foods for the treatment of rare diseases.

Hereditary Orotic Aciduria Market Segment Analysis:

Hereditary Orotic Aciduria Market is Segmented on the basis of Drug type, Distribution channel, Indication, and Region.

By Drug Type, the Uridine monophosphate segment is expected to dominate the market during the forecast period

-

The market of uridine supplementation segment is expected to have the highest market share during the forecast period. A precursor in the pathway of pyrimidine synthesis, uridine, is effective in overcoming the metabolic disorder due to the genetic enzyme deficiency seen in hereditary orotic aciduria. This selected treatment method has provided symptomatic relief where significant biochemical dysregulation occurs in the affected patients, which includes anemia, growth retardation, and developmental disorders. The efficacy of the drug and specificity of uridine usage in hereditary orotic aciduria together with relative certainty in the protocols of its usage have consolidated the role of such medication as the optimal one in the treatment of patients. Moreover, innovative formulation and methods of administrating uridine overwrite expectations to improve the treatment efficiency of this segment and strengthen it against other possible therapies in the niche patient population.

By Distribution Channel, Hospital segment expected to held the largest share

-

In the context of this study, the largest market share within the time frame of the forecast will be occupied by the hospital pharmacies segment for hereditary orotic aciduria treatments. As this metabolic disorder is rare and little can be done to manage this condition, treatments like uridine and other supportive therapies are usually recommended and given in medical care facilities mostly in hospitals. The hospital pharmacies suffice to prescribe these OPCs and monitor dosing and the special metabolisms that are inherent in hereditary orotic aciduria. Also, this type of patient needs constant control and regular check-ups, which also underlines the need for hospital pharmacies for treatment. During awareness of the disorder making people and families seek early diagnosis and treatment, the hospital setting's pharmacy retailing channel should remain prominent in distributing important medication to patients within a clinical setting.

Hereditary Orotic Aciduria Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

North America is expected to dominate the hereditary orotic aciduria market through the forecast period attributed to the existence of well-developed facilities for healthcare, increased awareness about rare metabolic disorders and favorable reimbursement policies. The United States more specifically contains a large number of specific genetic testing and diagnosis centers that facilitate early and accurate diagnosis of such rare diseases as hereditary orotic aciduria. Furthermore, North America’s well-developed research and development base and high concentration of large pharma and biotech firms work to progress treatments and therapies specific to rare diseases. This area has support from the government through policies that exist in individual countries for instance the Orphan Drug Act that prevails in the United States that provides tax credits, grants, and market exclusivity for a company that happens to be producing treatment for disorders that affect a small fraction of the population.

- In addition, several patient associations in North America that exists and include but are not limited to the National Organization for Rare Disorders (NORD) exist in a sole purpose of educating patients, supporting disease registries, and seeking funds for collecting disease-specific data for rare diseases. Organizations exist to facilitate the relationships between the patients, providers, and researchers to improve the treatment services and continuous improvement. In addition, the resource-rich reimbursement system is present in the region such as Medicaid and private insurance health plans to retain patients’ financial pressure to maintain respective genetic tests and specific therapies. With these factors in place, North America will keep on dominating the market as innovation in traditional genetic therapies and personalized medicine helps to determine the course of treating hereditary orotic aciduria.

Active Key Players in the Hereditary Orotic Aciduria Market:

-

AbbVie Inc. (United States)

- Aeglea BioTherapeutics, Inc. (United States)

- Alexion Pharmaceuticals, Inc. (United States)

- Amgen Inc. (United States)

- BioMarin Pharmaceutical Inc. (United States)

- Centogene N.V. (Germany)

- Cyclo Therapeutics, Inc. (United States)

- Enzyvant Therapeutics GmbH (Switzerland)

- Horizon Therapeutics plc (Ireland)

- Merck KGaA (Germany)

- Novartis AG (Switzerland)

- Orphazyme A/S (Denmark)

- Pfizer Inc. (United States)

- Recordati Rare Diseases Inc. (Italy)

- Sanofi S.A. (France)

- Other Active Players

Key Industry Developments in the Hereditary Orotic Aciduria Market:

-

In October 2023, an official signing ceremony for the Oxford-Harrington Rare Disease Centre Therapeutics Accelerator was held at the University of Oxford in October 2023, in conjunction with the Harrington Discovery Institute at University Hospitals in Cleveland, Ohio. The Oxford-Harrington Rare Disease Centre (OHC), a collaboration between the Harrington Discovery Institute and the University of Oxford formed in 2019, hosted the event. Leaders from OHC, the Harrington family, University Hospitals, Oxford Science Enterprises, and the University of Oxford were present for the signing.

|

Hereditary Orotic Aciduria Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 355.9 Million |

|

Forecast Period 2024-32 CAGR: |

4.7 % |

Market Size in 2032: |

USD 538.08 Million |

|

Segments Covered: |

By Drug Type |

|

|

|

By Distribution Channel |

|

||

|

By Indication |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Hereditary Orotic Aciduria Market by Drug Type

4.1 Hereditary Orotic Aciduria Market Snapshot and Growth Engine

4.2 Hereditary Orotic Aciduria Market Overview

4.3 Cytidine

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Cytidine: Geographic Segmentation Analysis

4.4 Uridine monophosphate

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Uridine monophosphate: Geographic Segmentation Analysis

Chapter 5: Hereditary Orotic Aciduria Market by Distribution Channel

5.1 Hereditary Orotic Aciduria Market Snapshot and Growth Engine

5.2 Hereditary Orotic Aciduria Market Overview

5.3 Hospital

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Hospital: Geographic Segmentation Analysis

5.4 Retail

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Retail: Geographic Segmentation Analysis

5.5 and Online Pharmacies

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 and Online Pharmacies: Geographic Segmentation Analysis

Chapter 6: Hereditary Orotic Aciduria Market by Indication

6.1 Hereditary Orotic Aciduria Market Snapshot and Growth Engine

6.2 Hereditary Orotic Aciduria Market Overview

6.3 Type 1 and Type 2

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Type 1 and Type 2: Geographic Segmentation Analysis

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Hereditary Orotic Aciduria Market Share by Manufacturer (2023)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ABBVIE INC. (UNITED STATES)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 AEGLEA BIOTHERAPEUTICS INC. (UNITED STATES)

7.4 ALEXION PHARMACEUTICALS INC. (UNITED STATES)

7.5 AMGEN INC. (UNITED STATES)

7.6 BIOMARIN PHARMACEUTICAL INC. (UNITED STATES)

7.7 CENTOGENE N.V. (GERMANY)

7.8 CYCLO THERAPEUTICS INC. (UNITED STATES)

7.9 ENZYVANT THERAPEUTICS GMBH (SWITZERLAND)

7.10 HORIZON THERAPEUTICS PLC (IRELAND)

7.11 MERCK KGAA (GERMANY)

7.12 NOVARTIS AG (SWITZERLAND)

7.13 ORPHAZYME A/S (DENMARK)

7.14 PFIZER INC. (UNITED STATES)

7.15 RECORDATI RARE DISEASES INC. (ITALY)

7.16 SANOFI S.A. (FRANCE)

7.17 OTHER ACTIVE PLAYERS

Chapter 8: Global Hereditary Orotic Aciduria Market By Region

8.1 Overview

8.2. North America Hereditary Orotic Aciduria Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By Drug Type

8.2.4.1 Cytidine

8.2.4.2 Uridine monophosphate

8.2.5 Historic and Forecasted Market Size By Distribution Channel

8.2.5.1 Hospital

8.2.5.2 Retail

8.2.5.3 and Online Pharmacies

8.2.6 Historic and Forecasted Market Size By Indication

8.2.6.1 Type 1 and Type 2

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Hereditary Orotic Aciduria Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By Drug Type

8.3.4.1 Cytidine

8.3.4.2 Uridine monophosphate

8.3.5 Historic and Forecasted Market Size By Distribution Channel

8.3.5.1 Hospital

8.3.5.2 Retail

8.3.5.3 and Online Pharmacies

8.3.6 Historic and Forecasted Market Size By Indication

8.3.6.1 Type 1 and Type 2

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Hereditary Orotic Aciduria Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By Drug Type

8.4.4.1 Cytidine

8.4.4.2 Uridine monophosphate

8.4.5 Historic and Forecasted Market Size By Distribution Channel

8.4.5.1 Hospital

8.4.5.2 Retail

8.4.5.3 and Online Pharmacies

8.4.6 Historic and Forecasted Market Size By Indication

8.4.6.1 Type 1 and Type 2

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Hereditary Orotic Aciduria Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By Drug Type

8.5.4.1 Cytidine

8.5.4.2 Uridine monophosphate

8.5.5 Historic and Forecasted Market Size By Distribution Channel

8.5.5.1 Hospital

8.5.5.2 Retail

8.5.5.3 and Online Pharmacies

8.5.6 Historic and Forecasted Market Size By Indication

8.5.6.1 Type 1 and Type 2

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Hereditary Orotic Aciduria Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By Drug Type

8.6.4.1 Cytidine

8.6.4.2 Uridine monophosphate

8.6.5 Historic and Forecasted Market Size By Distribution Channel

8.6.5.1 Hospital

8.6.5.2 Retail

8.6.5.3 and Online Pharmacies

8.6.6 Historic and Forecasted Market Size By Indication

8.6.6.1 Type 1 and Type 2

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Hereditary Orotic Aciduria Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By Drug Type

8.7.4.1 Cytidine

8.7.4.2 Uridine monophosphate

8.7.5 Historic and Forecasted Market Size By Distribution Channel

8.7.5.1 Hospital

8.7.5.2 Retail

8.7.5.3 and Online Pharmacies

8.7.6 Historic and Forecasted Market Size By Indication

8.7.6.1 Type 1 and Type 2

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Hereditary Orotic Aciduria Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 355.9 Million |

|

Forecast Period 2024-32 CAGR: |

4.7 % |

Market Size in 2032: |

USD 538.08 Million |

|

Segments Covered: |

By Drug Type |

|

|

|

By Distribution Channel |

|

||

|

By Indication |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||